Report Nº: 111316/03/2025

At the end of the month, the pension moratorium expires. It must not be renewed, but it is not a good idea to let it expire without doing something. The requirement of 30 years of contributions to receive a pension must be eliminated. This is the first fundamental step towards an integral organization of the pension system.

Once again, the pensioners’ cause resulted in serious acts of violence. On this occasion, the novelty was that the savagery in the name of the pensioners was carried out by soccer hooligans (“barras bravas”), organizations with a long history of coercion, crime, and destruction. Substantially, the violence observed did not differ much from what occurred in 2017, when Congress was dealing with the pension indexing rule.

A warning sign is the upcoming expiration of the pension moratorium at the end of March. Moratoriums are used by people who reach retirement age (60 women; 65 men) without the required minimum of 30 years of contributions. The mechanism consists of pretending to have been self-employed, for the missing years of contributions, to complete the minimum 30 years of contributions required by law. For this period of contributions not paid, a debt is calculated which is paid with installments deducted from the pension.

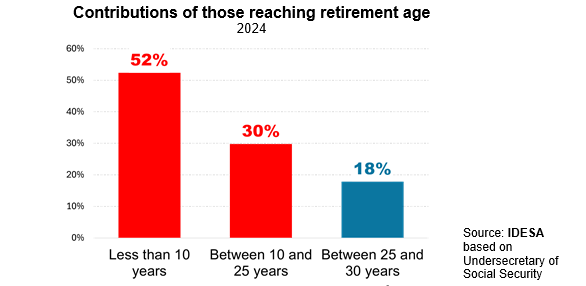

Approximately two-thirds of those who reach retirement age appeal to the moratorium because they do not comply with the minimum of 30 years of contributions. According to the Undersecretariat of Social Security among these people, by 2024, it is observed that:

These data show that there is a wide dispersion in the contribution density of people reaching retirement age. At one extreme, the majority accumulate less than 10 years of contributions. At the other extreme, only 2 out of every 10 people reach retirement age with less than 5 years to complete the minimum required by law. If the moratoriums are not renewed, all these people will have to postpone retirement or access the Universal Pension for the Elderly (PUAM). This is a non-contributory benefit with two important defects. The first is that it does not recognize contributions made under 30 years of age. In other words, a person with no contributions and another with 29 years of contribution receive the same PUAM. The second is that it does not allow to continue working, when contributory pensions do.

The requirement of 30 years of contributions comes from the time when the pension system was mixed, combining pay-as-you-go and capitalization. In the pay-as-you-go system, the requirement is 30 years of contributions, while in the funded system there was no minimum contribution requirement since people could retire whenever they wanted with the income derived from their capitalization account. When the capitalization regime was eliminated, the mistake was not revising this rule. Consequently, the requirement of a minimum of 30 years of contribution became for all benefits. As this barrier excludes most people, instead of correcting the mistake, moratoriums were established, deepening the pension system’s financial crisis and the injustice of delivering contributory pensions with no contribution.

The urgency now is to find a better alternative to the moratoriums. The moratoriums have been renewed for two decades, which has deepened the pension system’s degradation. A better alternative is to eliminate the minimum of 30 years of contribution. For people with few contributions, where the amount is very low, the PUAM should be considered the guaranteed floor. The amount of the PUAM should increase according to the accumulated contributions and the beneficiaries of the PUAM should be allowed to continue working if they want.

But the urgency should not obscure the importance of addressing an integral ordering of the pension system. Among the key points are the revision of the special and differential regimes, addressing the high litigiousness (there are 200,000 lawsuits by retirees against the State), reviewing the double coverage that occurs with widow pensions and providing for automatic adjustments to adapt the pension system to demographic changes.